Without much ado, here is the code

## Copyright (C) 2020 dekalog

##

## This program is free software: you can redistribute it and/or modify it

## under the terms of the GNU General Public License as published by

## the Free Software Foundation, either version 3 of the License, or

## (at your option) any later version.

##

## This program is distributed in the hope that it will be useful, but

## WITHOUT ANY WARRANTY; without even the implied warranty of

## MERCHANTABILITY or FITNESS FOR A PARTICULAR PURPOSE. See the

## GNU General Public License for more details.

##

## You should have received a copy of the GNU General Public License

## along with this program. If not, see

## .

## -*- texinfo -*-

## @deftypefn {} {@var{retval} =} market_profile_plot (@var{cross}, @var{n_bars})

##

## Plot a Market Profile Chart of CROSS of the last N_BARS.

##

## @seealso{}

## @end deftypefn

## Author: dekalog

## Created: 2020-05-11

function market_profile_plot( curr_cross , n_days )

pkg load statistics ;

cd /path/to/data/folder ;

price_name = tolower( curr_cross ) ;

if ( strcmp( price_name , 'aud_jpy' ) || strcmp( price_name , 'eur_jpy' ) || strcmp( price_name , 'gbp_jpy' ) || ...

strcmp( price_name , 'usd_jpy' ) )

tick_size = 0.001 ;

round_digit = 3 ;

elseif ( strcmp( price_name , 'xau_usd' ) )

tick_size = 0.1 ;

round_digit = 1 ;

elseif ( strcmp( price_name , 'xag_usd' ) )

tick_size = 0.01 ;

round_digit = 2 ;

else

tick_size = 0.0001 ;

round_digit = 4 ;

endif

## get price data of *_ohlc_10m

unix_command = [ "wc" , " " , "-l" , " " , [ price_name , '_ohlc_10m' ] ] ;

## the 'wc' with '-l' flag command counts the number of lines in [ price_name , '_ohlc_20m' ] }

[ ~ , system_out ] = system( unix_command ) ;

cstr = strsplit( system_out , " " ) ;

lines_in_file = str2double( cstr( 1 , 1 ) ) ;

## read *_ohlc_10m file

price_data = dlmread( [ price_name , '_ohlc_10m' ] , ',' , [ lines_in_file - ( n_days * 144 + 18 ) , 0 , lines_in_file , 21 ] ) ;

## get the earliest London open on a Sunday, if any

sun_open_ix = find( ( price_data( : , 11 ) == 1 ) .* ( price_data( : , 9 ) == 22 ) .* ( price_data( : , 10 ) == 0 ) ) ;

## get weekday closes

end_ix = find( ( price_data( : , 15 ) == 16 ) .* ( price_data( : , 16 ) == 50 ) ) ;

delete_ix = unique( [ sun_open_ix ; end_ix ] ) ;

## delete uuwanted data

price_data( 1 : delete_ix( 1 ) , : ) = [] ; end_ix = end_ix .- delete_ix( 1 ) ; open_ix = end_ix .+ 1 ;

end_ix( end_ix == 0 ) = [] ; end_ix( end_ix > size( price_data , 1 ) ) = [] ;

open_ix( open_ix == 0 ) = [] ; open_ix( open_ix > size( price_data , 1 ) ) = [] ;

## give names to data

open = price_data(:,18) ; high = price_data(:,19) ; low = price_data(:,20) ; close = price_data(:,21) ; vol = price_data(:,22) ;

high_round = floor( high ./ tick_size .+ 0.5 ) .* tick_size ;

low_round = floor( low ./ tick_size .+ 0.5 ) .* tick_size ;

max_tick_range = max( high_round .- low_round ) / tick_size ;

upper_val = high ; lower_val = low ;

## create y and x axes for chart

y_max = max( high_round ) + max_tick_range * tick_size ;

y_min = min( low_round ) - max_tick_range * tick_size ;

y_ax = ( y_min : tick_size : y_max )' ;

end_x_ax_freespace = 5 ;

## create container

all_vp = zeros( n_days , numel( y_ax ) ) ; all_mp = all_vp ;

if ( n_days == 1 )

[ all_vp(1,:) , vp_val ] = pcolor_background( y_ax , high , low , vol , tick_size ) ;

vp_z = repmat( all_vp( 1 , : ) , numel( high ) + end_x_ax_freespace , 1 ) ;

lower_val( : ) = vp_val( 1 ) ; upper_val( : ) = vp_val( 2 ) ;

elseif ( n_days >= 2 )

vp_z = zeros( numel( high ) + end_x_ax_freespace , size( all_vp , 2 ) ) ;

for ii = 1 : numel( end_ix )

[ all_vp(ii,:) , vp_val ] = pcolor_background( y_ax , high(open_ix(ii):end_ix(ii)) , low(open_ix(ii):end_ix(ii)) , ...

vol(open_ix(ii):end_ix(ii)) , tick_size ) ;

vp_z(open_ix(ii):end_ix(ii),:) = repmat( all_vp(ii,:)./max(all_vp(ii,:)) , numel( high(open_ix(ii):end_ix(ii)) ) , 1 ) ;

lower_val( open_ix(ii) : end_ix(ii) ) = vp_val( 1 ) ; upper_val( open_ix(ii) : end_ix(ii) ) = vp_val( 2 ) ;

endfor

[ all_vp(end,:) , vp_val ] = pcolor_background( y_ax , high(open_ix(end):end) , low(open_ix(end):end) , ...

vol(open_ix(end):end) , tick_size ) ;

vp_z( open_ix( end ) : end , : ) = repmat( all_vp( end , : ) ./ max( all_vp( end , : ) ) , ...

numel( high( open_ix( end ) : end ) ) + end_x_ax_freespace , 1 ) ;

lower_val( open_ix( end ) : end ) = vp_val( 1 ) ; upper_val( open_ix( end ) : end ) = vp_val( 2 ) ;

endif

## create the background ( best choices - viridis and ocean? )

x_ax = ( 1 : 1 : numel( open ) + end_x_ax_freespace )' ;

colormap( 'viridis' ) ; figure( 10 ) ; pcolor( x_ax , y_ax , vp_z' ) ; shading interp ; axis tight ;

## plot the individual volume profiles

hold on ;

scale_factor = ( 1 / max(max(all_vp) ) ) * 72 ;

for ii = 1 : numel( open_ix )

figure( 10 ) ; fill( all_vp( ii , : ) .* scale_factor .+ open_ix( ii ) , y_ax' , [99;99;99]./255 ) ;

endfor

## plot candlesticks

figure( 10 ) ; candle_mp( high , low , close , open ) ;

## plot upper and lower boundaries of value area

hold on ; figure( 10 ) ; plot( lower_val , 'b' , 'linewidth' , 2 , upper_val , 'r' , 'linewidth' , 2 ) ; hold off ;

## Plot vertical lines for London open at 7am

london_ix = find( ( price_data( : , 9 ) == 7 ) .* ( price_data( : , 10 ) == 0 ) ) ;

if ( ~isempty( london_ix ) )

for ii = 1 : numel( london_ix )

figure( 10 ) ; vline( london_ix( ii ) , 'g' ) ;

endfor

endif

endfunction

which calls this

## Copyright (C) 2020 dekalog

##

## This program is free software: you can redistribute it and/or modify it

## under the terms of the GNU General Public License as published by

## the Free Software Foundation, either version 3 of the License, or

## (at your option) any later version.

##

## This program is distributed in the hope that it will be useful, but

## WITHOUT ANY WARRANTY; without even the implied warranty of

## MERCHANTABILITY or FITNESS FOR A PARTICULAR PURPOSE. See the

## GNU General Public License for more details.

##

## You should have received a copy of the GNU General Public License

## along with this program. If not, see

## .

## -*- texinfo -*-

## @deftypefn {} {@var{vp_z}, @var{vp_val} =} pcolor_background (@var{y_ax}, @var{high}, @var{low}, @var{vol}, @var{tick_size})

##

## @seealso{}

## @end deftypefn

## Author: dekalog

## Created: 2020-05-13

function [ vp_z , vp_val ] = pcolor_background ( y_ax , high , low , vol , tick_size )

vp_z = zeros( 1 , numel( y_ax ) ) ; ##tpo_z = vp_z ;

vol( vol <= 1 ) = 2 ; ## no single point vol distributions

vp_val = zeros( 2 , 1 ) ;

for ii = 1 : numel( high )

## the volume profile, vp_z

ticks = norminv( linspace(0,1,vol(ii)+2) , (high(ii) + low(ii))/2 , (high(ii) - low(ii))*0.25 ) ;

ticks = floor( ticks( 2 : end - 1 ) ./ tick_size .+ 0.5 ) .* tick_size ;

unique_ticks = unique( ticks ) ;

if ( numel( unique_ticks ) > 1 )

[ N , X ] = hist( ticks , unique( ticks ) ) ;

[ ~ , N_ix ] = max( N ) ; tick_ix = X( N_ix ) ;

[ ~ , centre_tick ] = min( abs( y_ax .- tick_ix ) ) ;

vp_z(1,centre_tick-N_ix+1:centre_tick+(numel(N)-N_ix)) = vp_z(1,centre_tick-N_ix+1:centre_tick+(numel(N)-N_ix)).+ N ;

elseif ( numel( unique_ticks ) == 1 )

[ ~ , centre_tick ] = min( abs( y_ax .- unique_ticks ) ) ;

vp_z( 1 , centre_tick ) = vp_z( 1 , centre_tick ) + vol( ii ) ;

endif

endfor

[ ~ , vp_val_centre_ix ] = max( vp_z ) ;

sum_vp_cutoff = 0.7 * sum( vp_z ) ;

count = 1 ;

while ( count ~= 0 )

sum_vp_z = sum( vp_z( max( vp_val_centre_ix - count , 1 ) : min( vp_val_centre_ix + count , numel( vp_z ) ) ) ) ;

if ( sum_vp_z >= sum_vp_cutoff )

vp_val( 1 , 1 ) = y_ax( max( vp_val_centre_ix - count , 1 ) ) ; ## lower

vp_val( 2 , 1 ) = y_ax( min( vp_val_centre_ix + count , numel( vp_z ) ) ) ; ## upper

count = 0 ;

else

count = count + 1 ;

endif

endwhile

endfunction

and this

function hhh=vline(x,in1,in2)

% function h=vline(x, linetype, label)

%

% Draws a vertical line on the current axes at the location specified by 'x'. Optional arguments are

% 'linetype' (default is 'r:') and 'label', which applies a text label to the graph near the line. The

% label appears in the same color as the line.

%

% The line is held on the current axes, and after plotting the line, the function returns the axes to

% its prior hold state.

%

% The HandleVisibility property of the line object is set to "off", so not only does it not appear on

% legends, but it is not findable by using findobj. Specifying an output argument causes the function to

% return a handle to the line, so it can be manipulated or deleted. Also, the HandleVisibility can be

% overridden by setting the root's ShowHiddenHandles property to on.

%

% h = vline(42,'g','The Answer')

%

% returns a handle to a green vertical line on the current axes at x=42, and creates a text object on

% the current axes, close to the line, which reads "The Answer".

%

% vline also supports vector inputs to draw multiple lines at once. For example,

%

% vline([4 8 12],{'g','r','b'},{'l1','lab2','LABELC'})

%

% draws three lines with the appropriate labels and colors.

%

% By Brandon Kuczenski for Kensington Labs.

% brandon_kuczenski@kensingtonlabs.com

% 8 November 2001

if length(x)>1 % vector input

for I=1:length(x)

switch nargin

case 1

linetype='r:';

label='';

case 2

if ~iscell(in1)

in1={in1};

end

if I>length(in1)

linetype=in1{end};

else

linetype=in1{I};

end

label='';

case 3

if ~iscell(in1)

in1={in1};

end

if ~iscell(in2)

in2={in2};

end

if I>length(in1)

linetype=in1{end};

else

linetype=in1{I};

end

if I>length(in2)

label=in2{end};

else

label=in2{I};

end

end

h(I)=vline(x(I),linetype,label);

end

else

switch nargin

case 1

linetype='r:';

label='';

case 2

linetype=in1;

label='';

case 3

linetype=in1;

label=in2;

end

g=ishold(gca);

hold on

y=get(gca,'ylim');

h=plot([x x],y,linetype);

if length(label)

xx=get(gca,'xlim');

xrange=xx(2)-xx(1);

xunit=(x-xx(1))/xrange;

if xunit<0 .8="" code="" color="" else="" end="" g="=0" get="" h="" handlevisibility="" hhh="h;" hold="" if="" label="" nargout="" off="" set="" tag="" text="" vline="" x-.05="" x="" xrange="" y="">

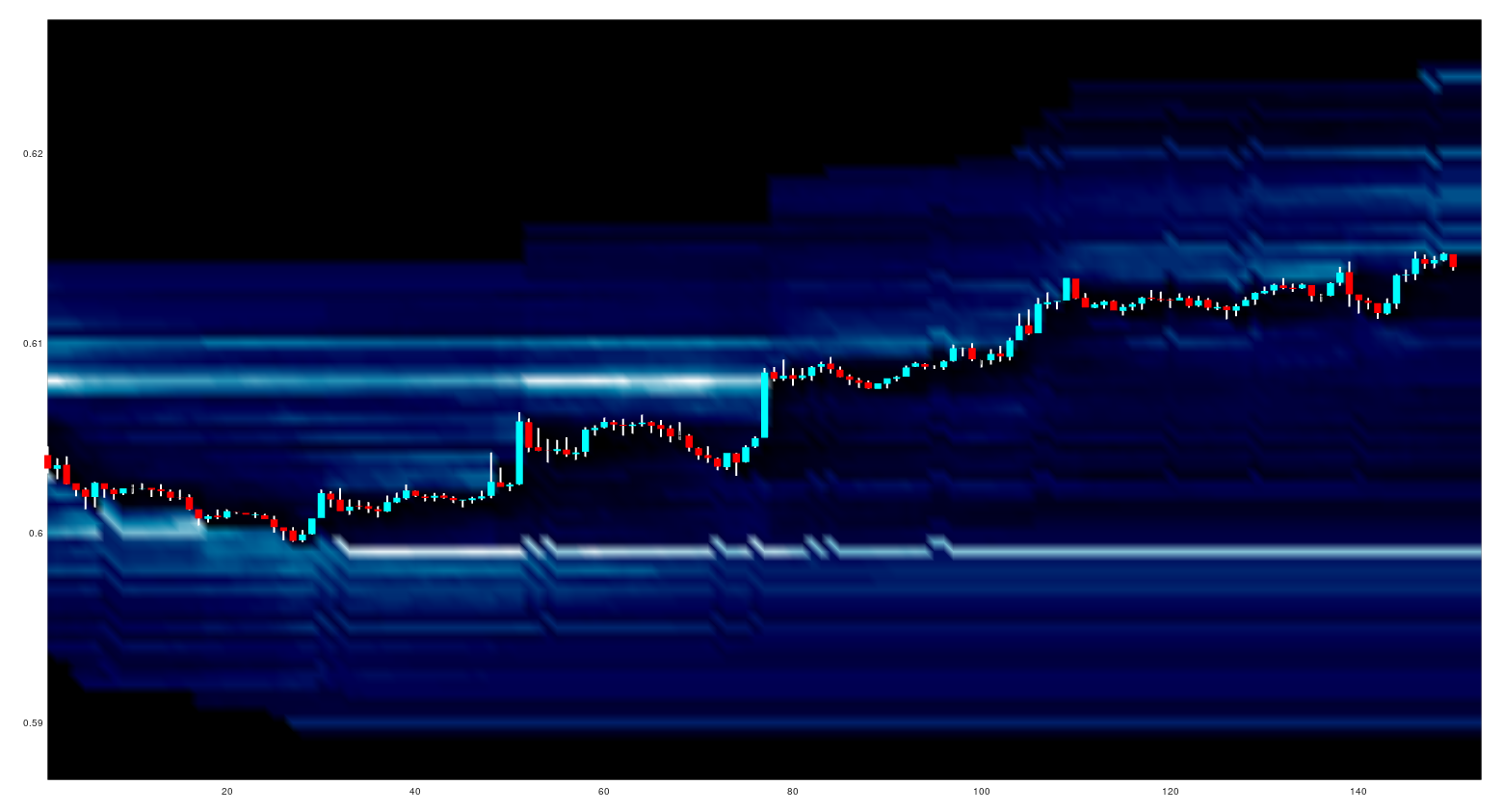

and produces charts such as this,

which is a 10 minute ohlc chart of the last 3 days, including "today's" ongoing price action. The number of days is a function input, and the horizontal blue and red lines indicate the upper and lower extremes of the value area. The vertical green lines indicate the London opening bar (7am BST) and each set of levels ends at the New York closing bar (5pm EST).

Further examples are last 10 days

and last month

Enjoy!

The black line is the underlying cyclic price and the red, blue and green lines are the mean weight model probabilities for cyclic peaks, troughs or neither respectively. Points where the peak/trough probabilities exceed the neither probabilities are marked by the red and blue vertical lines. Similarly, we have prices trending up in a cyclic fashion

The black line is the underlying cyclic price and the red, blue and green lines are the mean weight model probabilities for cyclic peaks, troughs or neither respectively. Points where the peak/trough probabilities exceed the neither probabilities are marked by the red and blue vertical lines. Similarly, we have prices trending up in a cyclic fashion and also trending down

and also trending down In the cases of the last two trending markets only the swing highs and lows are indicated. The reason for this is that during training, based on my "expert knowledge" of the cyclic tau features used, it is unreasonable to expect these features to accurately capture the end of an up leg in a bull trend or the end of a down leg in a bear trend - hence these were not presented as a positive class during training.

In the cases of the last two trending markets only the swing highs and lows are indicated. The reason for this is that during training, based on my "expert knowledge" of the cyclic tau features used, it is unreasonable to expect these features to accurately capture the end of an up leg in a bull trend or the end of a down leg in a bear trend - hence these were not presented as a positive class during training.